Charitable giving rules just had their biggest overhaul in years. The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, introduced changes that expand the tax benefits of giving to millions of donors who previously had no direct incentive. Most donors and many nonprofit teams are still catching up on what changed and what it means for them.

501(c)(3) donation rules are the IRS requirements governing tax-deductible charitable contributions to qualifying nonprofit organizations, including deductibility limits, substantiation standards, and how donated funds may be restricted or unrestricted.

This guide covers the core rules, the 2026 OBBBA changes, a new 2027 scholarship credit, and how your nonprofit can communicate all of it to the right donors at the right time.

Tax Disclaimer: This content is for informational purposes only and does not constitute tax or legal advice. Tax laws change frequently. Consult a qualified tax professional before making donation-related decisions. Last Updated: [June 2026] — reviewed annually each September.

What Is a 501(c)(3) Organization?

A 501(c)(3) organization is a nonprofit entity recognized by the IRS as tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Qualified contributions to 501(c)(3) organizations may be deducted as charitable contributions on a donor’s federal income tax return, subject to IRS requirements.

The two main types of 501(c)(3) organizations carry different deduction limits, and donors should know the difference.

Public charities

Public charities include the broad category of nonprofits most people interact with: schools, hospitals, community organizations, religious institutions, and arts groups. Cash contributions to public charities are deductible up to 60% of the donor’s adjusted gross income (AGI), per IRS Publication 526.

Private foundations

Private foundations are typically funded by a single individual, family, or corporation. Cash contributions to private foundations are deductible up to 30% of AGI, a less favorable limit for large donors. Note that the 2026 universal deduction (discussed below) does not apply to gifts to private foundations.

To verify whether an organization currently qualifies for tax-deductible contributions before donating or issuing acknowledgments, use the IRS Tax Exempt Organization Search at IRS.gov.

What Are the 501(c)(3) Donation Rules & Documentation Requirements?

Several IRS requirements apply to charitable contributions regardless of recent law changes. These are the five foundational donation rules and requirements every donor and nonprofit should know.

1. Who can deduct

Prior to 2026, only taxpayers who itemized deductions could deduct charitable contributions. Beginning in 2026, non-itemizers also have access to a deduction under the OBBBA. Read more on each group’s rules in the OBBBA section below.

2. AGI deduction limits.

The ceiling on how much a donor can deduct in a given year depends on the type of gift and the type of organization receiving it:

| Contribution Type | AGI Deduction Limit |

| Cash to public charities | Up to 60% of AGI |

| Cash to private foundations | Up to 30% of AGI |

| Appreciated capital gains property | Up to 30% of AGI |

Contributions exceeding the applicable AGI limit in one year may generally be carried forward for up to five years, subject to the same percentage limits in each subsequent year. Verify specific carryforward rules with a tax professional, as new OBBBA floors may affect how carried amounts are treated.

3. Written acknowledgment for gifts of $250 or more

According to IRS.gov, donors may not claim a deduction for any single contribution of $250 or more without a contemporaneous written acknowledgment from the nonprofit.

A nonprofit acknowledgment letter must include:

- Organization’s name

- Date of the donor contribution

- Amount of cash donated or a description of any non-cash property

- Statement of whether goods or services were provided in exchange, along with a good-faith estimate of their value if applicable. If nothing was provided in return, the letter should say so explicitly.

4. Quid pro quo contributions

When a donor gives more than $75 and receives something of value in return, the nonprofit must provide a written disclosure including a good-faith estimate of the fair market value of what the donor received, according to IRS.gov. Failure to provide this disclosure may result in penalties.

5. Form 8283 for non-cash gifts

Non-cash contributions above $500 require donors to file Form 8283. Gifts above $5,000 generally require a qualified appraisal.

There have always been consistent best practices in fundraising—issuing acknowledgments promptly after each gift, retaining copies, and using consistent templates that include all required elements. Choose a donor management software that consistently automates rules and acknowledgments wherever possible. Automations reduce human errors, free up your development team’s time, and support donor compliance.

What Is the Difference Between Restricted and Unrestricted Donations?

Restricted donations are gifts where the donor designates a specific purpose for the funds, such as a particular program, scholarship, building project, or geographic region. Nonprofits that accept restricted gifts are legally obligated to honor those conditions. Restricted funds must be tracked separately in financial records and reported appropriately on Form 990. Accepting a gift with conditions the organization cannot or will not fulfill creates real legal and reputational risk.

Unrestricted donations give the organization full discretion to direct funds where they are needed most. They are operationally flexible and valuable, but often harder to fundraise for, because donors tend to feel more engaged when they can connect their gift to a specific outcome. Strong impact storytelling is the most effective way to attract unrestricted support.

A written gift acceptance policy helps organizations manage both types consistently. It defines which types of restricted gifts the organization will and will not accept, reducing the risk of receiving gifts with conditions that are impractical, legally problematic, or misaligned with the nonprofit’s mission.

Managing restricted and unrestricted contributions in organized, accessible records also simplifies year-end acknowledgment and Form 990 reporting. GiveSmart by Momentive Software offers donor management tools including giving history tracking, donor segmentation, and automated acknowledgment to help development teams stay organized and compliant.

What Changed in 2026: New OBBBA Tax Rules Every Donor Should Know

The One Big Beautiful Bill Act, signed July 4, 2025, made the most significant changes to federal charitable deduction rules in years. Most provisions took effect January 1, 2026. Here is what changed and what it means in practice.

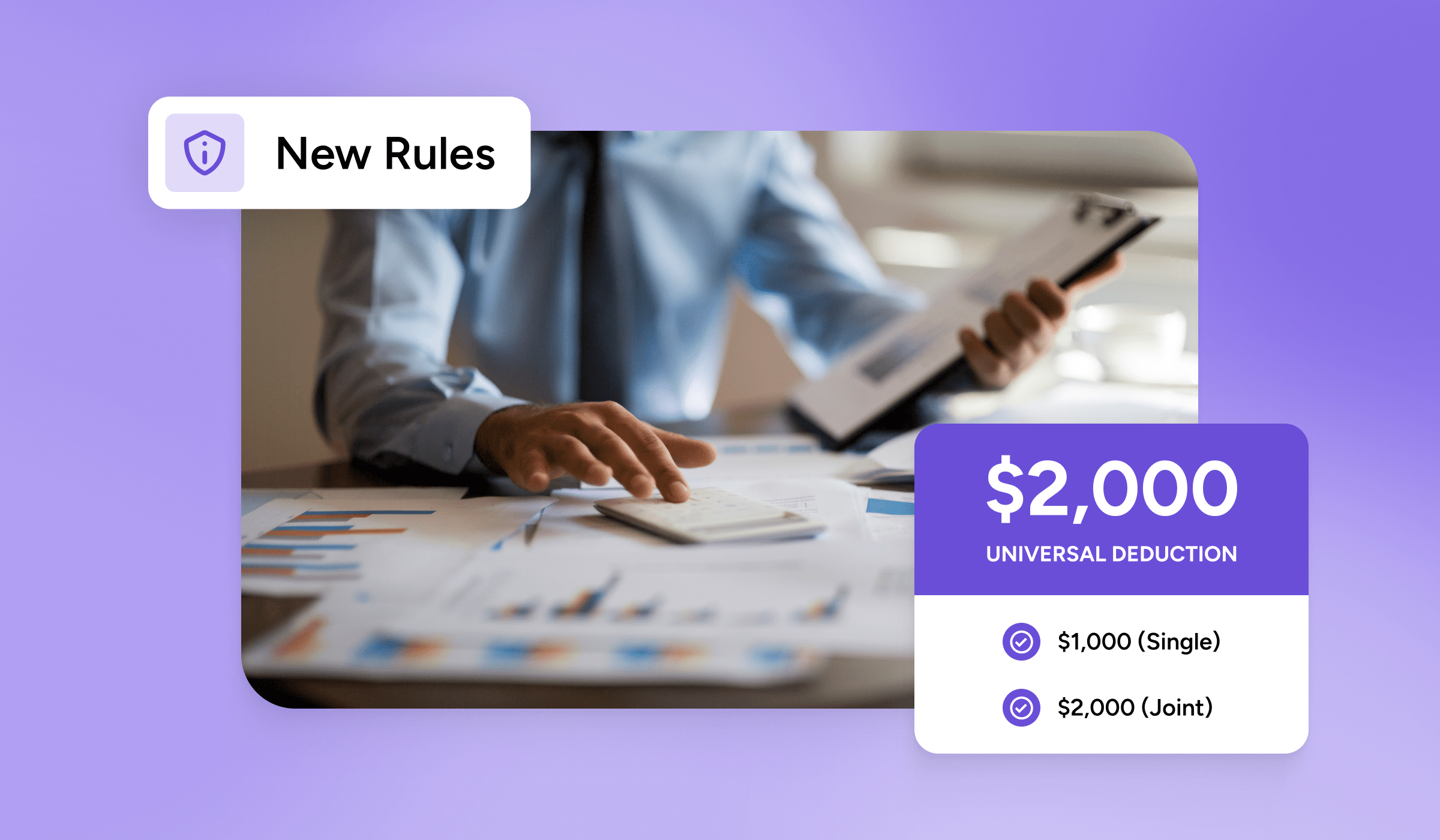

Universal Charitable Deduction Returns for Non-Itemizers

Beginning in the 2026 tax year, taxpayers who take the standard deduction may claim an above-the-line charitable deduction of up to $1,000 (single filers) or $2,000 (married filing jointly) for cash donations to qualifying public charities, according to the OBBBA. This deduction does not apply to gifts to donor-advised funds, supporting organizations, or private foundations.

This is a major shift. As Fidelity Charitable notes, roughly 90% of households take the standard deduction, meaning the vast majority of American taxpayers have had no direct tax incentive to give since the Tax Cuts and Jobs Act of 2017 significantly raised the standard deduction. That changes in 2026.

For nonprofits, the message to standard filers is simple and powerful: for the first time in years, your donation to our organization can lower your tax bill, even if you don’t itemize.

Changes for Itemizers and High-Income Donors

Taxpayers who itemize deductions face two new rules beginning in 2026, per the OBBBA.

First, a 0.5% AGI floor applies to charitable deductions for all itemizers. Only the portion of charitable contributions that exceeds 0.5% of the donor’s adjusted gross income is deductible. For a donor with an AGI of $200,000, that means only gifts above $1,000 produce a deduction. Amounts that fall below the floor do not generate a deduction in the contribution year. Amounts below the floor do not generate a deduction in the year of contribution; however, according to the IRS Publication 505, they are added to the charitable contribution carryover and may be deductible in future tax years, subject to the same rules.

Second, for taxpayers in the top 37% federal income tax bracket, all itemized deductions, including charitable contributions, are effectively valued at 35 cents per dollar rather than 37 cents per the OBBBA (confirmed by IRS Revenue Procedure 2025-32). The net tax benefit per donated dollar is reduced for the highest earners.

For major donor conversations, these changes are worth acknowledging directly. Strategies such as bunching multiple years of planned gifts into a single tax year to clear the 0.5% floor, or contributing to a donor-advised fund, can preserve the tax value of a major gift.

New Corporate Giving Threshold

Beginning in 2026, corporations face a new 1% of taxable income floor on charitable deductions, under IRC Section 170(b)(2)(A) as amended by the OBBBA. Contributions that do not exceed 1% of the corporation’s taxable income are nondeductible. The existing 10% ceiling on corporate charitable deductions remains in place.

For development staff, this is an opportunity to reframe corporate partnership conversations. A small gift that no longer carries a tax benefit becomes an invitation to a deeper, more strategic relationship.

Estate Planning and Legacy Giving

The OBBBA permanently raised the federal estate and gift tax exemption to $15 million per individual and $30 million for married couples, effective January 1, 2026, according to the OBBBA and confirmed by estate planning practitioners.

With fewer estates subject to federal estate tax under the new thresholds, legacy giving conversations shift away from tax planning and toward values and impact. That is a more durable message. A donor who gives because they care about the mission, not just to reduce an estate tax bill, is a stronger long-term partner.

The 2027 Scholarship Tax Credit: What K-12 Nonprofits Need to Know

The OBBBA created a new Federal Scholarship Tax Credit (FTSC) for contributions to Scholarship Granting Organizations (SGOs). This provision takes effect January 1, 2027, not 2026. Nonprofits communicating about tax benefits should be precise about this timing to avoid donor confusion.

Beginning with the 2027 tax year, individual taxpayers may claim a nonrefundable federal tax credit of up to $1,700 for cash contributions to qualified SGOs. The credit is per taxpayer, meaning spouses filing jointly may each claim up to $1,700. Because the credit is nonrefundable, it reduces tax liability dollar-for-dollar but cannot exceed what the donor owes.

The distinction between a credit and a deduction is worth explaining clearly to donors. A deduction reduces taxable income; its value depends on the donor’s tax bracket. A credit reduces the actual tax owed, dollar-for-dollar, regardless of bracket. For many donors, the $1,700 credit will effectively make the contribution cost-neutral from a tax standpoint.

State participation is required. According to IRS Revenue Procedure 2026-6, a state must elect to participate and provide the IRS with a certified list of qualifying SGOs before contributions to those organizations can generate the credit. States making advance elections for 2027 use Form 15714. Contributions to SGOs in states that have not elected to participate do not qualify.

For K-12 nonprofits: if your state participates and your organization qualifies as an SGO, start communicating this credit to donors now, clearly labeled as a 2027 opportunity. Early awareness lets donors plan ahead.

How Nonprofits Should Communicate These Changes to Donors

The 2026 tax changes affect different segments of your donor base in different ways. A one-size message misses the opportunity to tailor messaging to each group and guide them towards the choices that make the most impact.

Address Everyday Donors Who Take the Standard Deduction

Lead with the universal deduction. For example, the messaging includes: “Starting in 2026, even if you take the standard deduction, your cash donation to [Organization Name] may qualify for a federal tax deduction of up to $1,000 per person. Your support goes even further this year.”

Acknowledge Major Donors Who Itemize

Acknowledge the new rules, then redirect to impact and giving options. For example: “As tax rules around large gifts have changed in 2026, we’d welcome a conversation about approaches that work best for your goals, whether that’s a direct gift, a donor-advised fund, or a charitable trust.”

Reframe New Rules for Corporate Partners

Reframe the new 1% floor as an invitation to a more intentional relationship. For example: “We’d love to explore a giving program that reflects your company’s impact goals and aligns with your revised corporate giving strategy for 2026.”

Lead with Values for Legacy and Estate Planning Prospects

The higher estate tax exemption reduces urgency around tax-driven estate planning, but opens values-driven legacy conversations. For example: “With estate tax thresholds now higher and permanent, many donors are focusing on the legacy they want to leave. We’d love to talk about how a bequest or planned gift could reflect your values and make a lasting difference.”

Update Your Materials Now

Acknowledgment letters should be reviewed to confirm they include all required elements per current IRS rules. Donation forms and campaign pages can incorporate language about the new standard-filer deduction. Year-end email campaigns benefit from segmentation so each donor group receives a message relevant to their giving profile.

What’s the guiding principle to communicating with donors? Lead with mission impact, not tax mechanics. The mission is the reason to give at all. Tax benefits are a reason to act now.

FAQ: 501(c)(3) Donation Rules

What are the IRS rules for donating to a 501(c)(3)?

Qualified contributions to 501(c)(3) organizations may be deducted on a federal income tax return, subject to AGI limits and substantiation requirements. Cash contributions to public charities are deductible up to 60% of adjusted gross income, per IRS Publication 526. Beginning in 2026, both itemizers and non-itemizers may claim a deduction under the OBBBA, though different rules apply to each group. Donors should verify an organization’s current 501(c)(3) status using the IRS Tax Exempt Organization Search at IRS.gov before claiming a deduction.

Can donors deduct without itemizing in 2026?

Yes. Under the One Big Beautiful Bill Act (signed July 4, 2025), non-itemizers may deduct cash donations of up to $1,000 for single filers or $2,000 for married couples filing jointly beginning in the 2026 tax year, per the OBBBA. This applies only to cash gifts made directly to qualified public charities and does not include gifts to donor-advised funds, private foundations, or supporting organizations. According to Fidelity Charitable, roughly 90% of households take the standard deduction, making this one of the most significant expansions of charitable giving incentives in years.

What documentation does a nonprofit need to provide?

For any single contribution of $250 or more, the nonprofit must provide a contemporaneous written acknowledgment that includes: the organization’s name, the date, the amount given or description of property, and a statement about whether any goods or services were provided in return, per IRS.gov. For quid pro quo contributions over $75, a written disclosure with a fair market value estimate of benefits received is required. For non-cash gifts over $500, the nonprofit signs the acknowledgment section of Form 8283.

What is the difference between restricted and unrestricted donations?

A restricted donation is a gift where the donor specifies how the funds must be used, such as for a particular program or project. An unrestricted donation gives the organization full discretion over the use of funds. Nonprofits must honor restricted gift terms, track the funds separately, and report them appropriately on Form 990. Unrestricted gifts offer greater operational flexibility but often require stronger impact communication to attract.

What is the $1,700 scholarship tax credit?

The Federal Scholarship Tax Credit is a nonrefundable credit of up to $1,700 per taxpayer for cash contributions to qualified scholarship granting organizations (SGOs), created by the OBBBA. It takes effect for tax year 2027, meaning it is first claimable when filing 2027 taxes in 2028, per IRS.gov. States must elect to participate and certify qualifying SGOs. Unlike a deduction, this credit reduces a donor’s tax liability dollar-for-dollar, up to the $1,700 limit per taxpayer.

How does the new corporate giving rule affect donations?

Under the OBBBA, corporations must make charitable contributions exceeding 1% of taxable income before any charitable deduction applies, beginning in 2026, per IRC Section 170(b)(2)(A). Contributions below the floor are nondeductible in the contribution year. The existing 10% ceiling on corporate charitable deductions remains in effect. Corporations with small or fragmented giving programs should review their strategy with a tax professional and consider whether consolidating giving improves their deduction eligibility.